MiCA: Europe’s New Crypto Regulations Will Transform Markets

This article was co-authored together with Dante Disparte and first published on the Bretton Woods Committe on July 1st 2024.

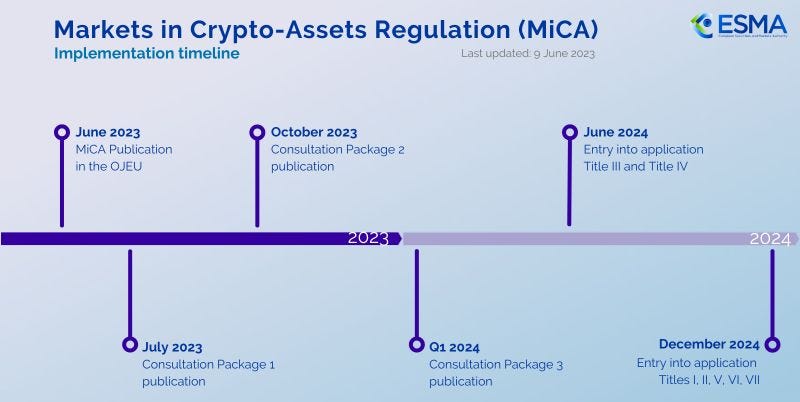

The year 2024 marks a major milestone for the crypto industry within the European Union and beyond as MiCA (Markets in Crypto-Assets Regulation) enters into application. This groundbreaking regulatory framework, regarded as the most comprehensive globally, is set to overhaul the crypto landscape with key implementation dates of June 30 for stablecoins and December 30 for Crypto Asset Service Providers (CASPs).

The journey to MiCA's implementation was spurred by notable events such as the Facebook-backed Libra project launched in 2019 or the Initial Coin Offering (ICO) craze in 2017, which highlighted the need for regulatory clarity to foster responsible innovation while preventing fraud and financial stability risks. After years of legislative deliberations, negotiations, and even a near-ban on Bitcoin trading in the EU, MiCA coming into force is now a reality - affording European crypto asset markets legal and regulatory clarity, which begs the question will other major jurisdictions follow Europe’s example?

It is also worth asking whether broader crypto market participants are ready for MiCA’s onset, or did they mistakenly treat MiCA like Y2K - a probable event with no consequence, or a serious deadline that would radically transform crypto market structure.

As MiCA's provisions take effect, it is reasonable to expect a transformative year ahead. In short, MiCA could be to crypto assets, what GDPR was to privacy.

How will the EU crypto market change?

The EU crypto market structure is anticipated to undergo substantial transformation. The market is projected to localize, institutionalize, professionalize and likely consolidate, as evidenced by Robinhood’s recent acquisition of Bitstamp. While the depth and breadth of MiCA’s impact may still be unseen, there are indeed significant changes underway.

Stablecoin offerings, both local and global, will either comply or ultimately vanish from the EU market in the short to mid term, as evidenced by recent announcements from exchanges like Binance, Bitstamp, Kraken, OKX and others that are either delisting or phasing out non-compliant tokens. More such announcements will follow as the year progresses and the reality sets in that the EU is now a zero-tolerance market for loosely regulated “internet funny money.”

Responsible actors who did not take the onset of MiCA as mere “regulatory theater” spent years preparing for it. MiCA represents an opportunity, notwithstanding certain limitations or excessive regulatory protectionism evident in the law, to grow a uniquely European crypto asset market. This includes potential growth and competition for Euro-denominated stablecoins, while on-shoring and passporting dollar-denominated equivalents, which currently are the digital thrift in crypto markets. A critical market improvement under MiCA is how the crypto asset value chain, from token issuers, to exchanges and, ultimately, custodial wallet providers (crypto asset services providers or CASPs in MiCA parlance) must all align to protect consumers and broader markets.

The stablecoin market in the EU will consolidate around regulated tokens, and the exchange market will follow suit. Foreign, unregulated exchanges will face significant restrictions, making it exceedingly difficult, if not impossible, to operate on a reverse solicitation basis. Entities that manage to overcome these regulatory hurdles are likely to gain market share, leading to a consolidated and robust market landscape. EU leadership in bringing crypto asset markets into the regulatory perimeter forces a broader race to the top in global crypto markets and raises a strategic opportunity for regulatory harmonization and equivalence.

The token issuance framework under MiCA, which extends beyond stablecoins, will attract global teams by offering clear and practical issuance standards, mitigating the regulatory uncertainty and enforcement risks prevalent in other regions. Furthermore, the overall EU market structure will benefit from strong protections against market abuse and insider trading, akin to those in traditional finance, which have been notably absent in the crypto realm until now. Indeed, many other countries are doing with often insidious enforcement actions what can otherwise be resolved with better consumer-facing disclosures. MiCA’s requirement that token issuer white papers carry legal and regulatory weight akin to an investor prospectus, is a good example of these new standards at work.

All of these changes will trigger a massive transformation with real business impact in the EU crypto market, which through the course of this year will accelerate EU competitiveness in digital assets. Nonetheless, significant open questions remain. For instance, there is uncertainty regarding the dual categorization of e-money tokens as both crypto-assets and e-money, the final publication and application of technical standards (often referred to as level two legislation), or the specific disclosure and liability obligations for exchanges, as well as how crypto assets are allowed (or encouraged) to interact with the real economy. No regulatory regime this far reaching is free from gaps, which has led some EU policymakers to contemplate MiCA 2.0, which would potentially address non-fungible tokens (NFTs) and decentralized finance (DeFi), among other areas.

As we emphasized 18 months ago, the ultimate measure of MiCA’s success will be its practical implementation and impact. When we look back on this transformational regulatory moment, what will matter most is how effective MiCA has been in enabling a unique European crypto asset market to flourish. A substantial portion of the implementation work still lies ahead, including developing supervisory guidance on individual open questions and establishing a consistent and workable approach across the 27 EU member states. MiCA undoubtedly presents a tremendous opportunity for the EU, but it will require the concerted and shared efforts of industry, regulators, policymakers, and ultimately, the nearly 450 million consumers to fully realize its potential.

Will MiCA have an impact on U.S. crypto policy developments?

MiCA's influence extends far beyond the EU’s borders, reaching industry actors and national regulators worldwide. As crypto rules are implemented in one of the largest markets globally, other stakeholders cannot afford to ignore its implications. MiCA standards are poised to shape business practices and emerging regulations on an international scale. The longer the regulatory vacuum for crypto persists in the U.S. and UK as two key jurisdictions, the greater the global impact of MiCA standards is likely to be. Now more than ever, not only with a backdrop of conflict in Europe, but also with a demand to future-proof trans-Atlantic economic ties, regulatory harmonization and technological competitiveness are twin pillars of U.S.-EU policy. The same should hold true across the English Channel, notwithstanding lingering Brexit tensions.

While MiCA has the potential to become an almost globally adopted regulatory standard this outcome is not guaranteed as more and more countries create bespoke crypto rules. Certain MiCA requirements, especially those pertaining to stablecoins and so-called significant stablecoins such as the proportion of reserve funds mandated to be held as bank deposits, may need to be revisited to avoid unintended consequences - including the risk of spillover effects from banks to fully-reserved stablecoin offerings. The U.S. should leverage the EU's experience and adopt payment stablecoin regulations promptly to maintain global competitiveness, while ensuring passportability and regulatory equivalence, especially where dollar-denominated stablecoins, like the dollar itself, play a dominant role in international crypto markets.

Ultimately, a coordinated approach among the U.S., the EU, and other major jurisdictions will be essential to pave the way for future regulatory recognition and to ensure an emerging internet financial system is rules-based.

Source: ESMA, MICA implementation timeline.