Analyzing MiCA's Significance Regime for Stablecoins

This article was first published on the Circle policy blog on February 14th 2024.

The emergence of global stablecoins has prompted both national and international regulatory bodies to examine their potential effects on financial stability and monetary sovereignty. Thus far, this concept has been largely theoretical in nature, with the exception of the collapse of Terra Luna’s so-called algorithmic ‘stablecoin’ - UST, that wiped out $40 billion in value virtually overnight (at its peak Lehman Brothers had a market value of $46 billion), but without affecting broader financial markets at any level.

The dramatic collapse of UST has sparked debates about the point at which stablecoins achieve global significance or systemic importance, thereby necessitating adjustments in regulation and oversight. In the absence of extensive practical experience and historical data, regulators have been confronted with the challenging responsibility of formulating functional and suitable rules for implementation.

The EU, rather characteristically, has been the first major jurisdiction to adopt a supervisory and regulatory regime for “significant stablecoins” in the Markets in Crypto-Asset Regulation (“MiCA”) that was passed in June 2023. Under MiCA, fiat-backed stablecoins or e-money tokens that have surpassed a specified adoption threshold, measured by a set of seven quantitative and qualitative indicators, will face additional and significantly increased regulatory requirements. At this point, they will also fall under the supervision of the European Banking Authority (EBA) as opposed to one of the EU’s national authorities.

Does this new regime appropriately capture and address the impact of global stablecoins?

Given the scarcity of historical precedents, it is logical to examine the existing frameworks in banking and payments that define the notion of "systemic importance" as a means to address this question effectively. This is precisely what Helmut Bauer, the former Head of Banking Supervision at German regulator BaFin, and I sought to achieve in our newly published report on MiCA’s significance regime - accessible through SSRN here.

Comparing MiCA’s regime for significant stablecoins with the Basel Committee on Banking Supervision (BCBS) framework for global systemically important banks (G-SIBs), the European Central Bank (ECB) oversight framework for electronic Payment Instruments, Schemes and Arrangements (PISA), and the EU Single Supervisory Mechanism (SSM) Framework for significant credit institutions in the EU, results in two main takeaways:

Firstly, what sets MiCA's regime apart is its dual-purpose approach: it not only transfers supervisory responsibility but also applies additional prudential measures. This is a unique feature not found in any other framework we've analyzed.

Second, while the transfer of supervisory responsibility to the EBA seems broadly aligned with the SSM framework and PISA who trigger EU supervision, MiCA’s significance criteria seem misaligned with the BCBS G-SIB model that is similarly aimed at capturing systemic risks and introducing increased prudential requirements. As one example, MiCA’s market capitalisation threshold sits at €5 billion, while the smallest G-SIB in terms of its size score assigned to G-SIB bucket 1 is Standard Chartered with a total value of assets of (GBP) £682 billion (end-2022).

This brings us to a nuanced conclusion. While the regime and the calibration of its significance thresholds may warrant the transfer of supervisory responsibility to the EBA, it does not appropriately represent systemic risk at the financial stability level that would warrant the substantial increase of prudential requirements similar to that of G-SIBs. Therefore, we propose that the dual purpose of MiCA’s significance regime should be disentangled.

To dig deeper into the comparison between MiCA’s significance regime and the BCBS G-SIB, the ECB PISA, and the EU SSM frameworks, as well the EU’s singular approach on the topic compared to the rest of the world, I encourage you to read the longer report here.

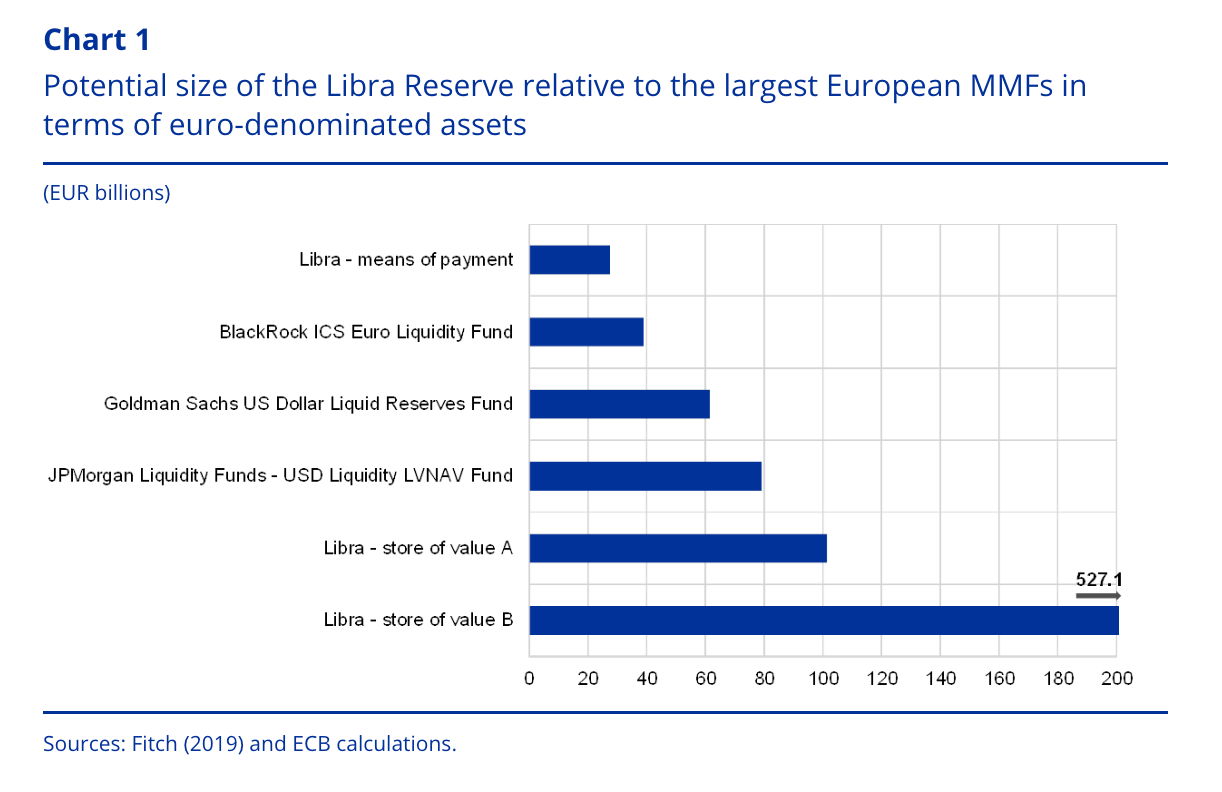

Source: ECB, A regulatory and financial stability perspective on global stablecoins, May 2020.